- UPSC Exam

- State PCS

- One Day Exam

- Current Affairs

- PT Quiz

- Downlaods

- About Coaching

- Blog

- Videos

| Prelims : (Economy + CA) Mains : (GS 2 – Welfare Schemes; GS 3 – Financial Inclusion, Labour Welfare) |

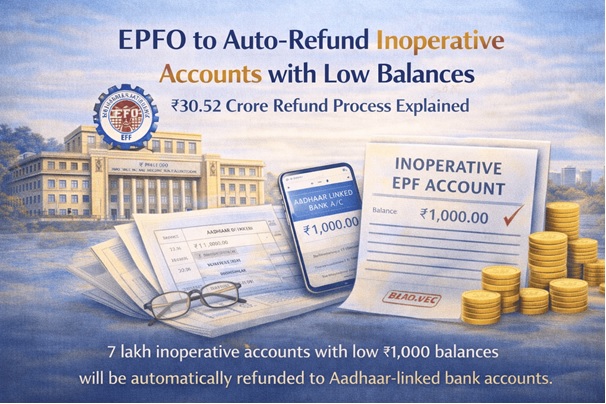

The Employees’ Provident Fund Organisation (EPFO) has approved auto-settlement of small inoperative Provident Fund (PF) accounts with balances of ₹1,000 or less. The decision was taken during the 239th meeting of the Central Board of Trustees (CBT).

This step aims to address the growing number of dormant accounts and ensure that small unclaimed balances are automatically transferred to members’ bank accounts linked with Aadhaar and EPFO records.

India’s formal workforce benefits from a statutory retirement savings system known as the Employees’ Provident Fund (EPF). The scheme was created to provide long-term financial security to workers in the organised sector.

The EPF operates under the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952 and is administered by the Employees’ Provident Fund Organisation (EPFO).

The scheme plays a crucial role in ensuring income security after retirement for millions of workers.

The Employees’ Provident Fund Organisation is a statutory body under the Government of India responsible for managing provident fund and pension schemes.

It is governed by the Central Board of Trustees (CBT), which includes representatives from the government, employers, and employees.

The organisation manages three key social security schemes :

The EPFO operates through a nationwide network of 147 offices across India to administer these schemes and provide services to workers and employers.

An inoperative EPF account refers to a provident fund account in which no interest is credited after a specified period due to inactivity.

An EPF account typically becomes inoperative when :

However, if the member is below 55 years of age, the account continues to earn interest until the age of 58, even if no contributions are made.

As of March 31, 2025, the EPFO recorded :

These figures exclude accounts belonging to international workers.

The large number of dormant accounts highlights challenges such as :

To address the issue of dormant accounts, the Central Board of Trustees of EPFO approved a pilot project for auto-settlement of inoperative accounts with small balances.

The initial phase will cover :

If the pilot project proves successful, the auto-settlement system may later be extended to accounts with balances above ₹1,000.

The EPFO is one of the largest social security organisations in the world.

The organisation manages a massive corpus exceeding ₹28.34 lakh crore.

Among the 31.83 lakh inoperative accounts, inactivity periods vary significantly.

These figures show that many provident fund accounts remain unclaimed for long periods.

The analysis of inoperative accounts also reveals a significant imbalance in fund distribution.

Most inoperative accounts contain relatively small balances.

In contrast, a small number of accounts contain a large share of funds.

This indicates that substantial amounts remain locked in a limited number of dormant accounts.

To implement the auto-settlement mechanism effectively, the EPFO conducted a Know Your Customer (KYC) verification exercise.

The pilot project focuses on accounts that meet the following criteria :

The analysis identified :

These accounts will be eligible for automatic settlement.

The EPFO is conducting a pilot validation study across 10 regional offices.

The pilot will examine accounts with balances up to ₹50,000 to evaluate operational feasibility.

For balances above ₹1,001, the following accounts have been identified :

These accounts may be included in future phases of the auto-settlement programme.

The initiative helps ensure that workers receive their rightful savings without complex claim procedures, particularly for small balances.

Automatic settlement reduces the workload of EPFO offices by eliminating the need for manual claim processing for small accounts.

Large amounts of retirement savings remain unclaimed in inactive accounts. The initiative helps return these funds to beneficiaries.

The use of Aadhaar-linked bank accounts and digital verification systems supports the government’s push toward transparent and efficient service delivery.

By simplifying withdrawal processes, the policy may increase public confidence in statutory social security schemes.

Despite its benefits, the initiative faces several challenges :

Outdated contact details and incomplete KYC records may limit successful auto-settlement.

Many workers may remain unaware of their EPF balances and entitlements.

Large-value dormant accounts may require additional verification before settlement.

Frequent job changes can result in multiple PF accounts, complicating fund consolidation.

To address the issue of dormant provident fund accounts more effectively, the following measures may be considered :

These measures could significantly improve the efficiency and accessibility of India’s social security framework.

FAQs1. What is the Employees’ Provident Fund (EPF) ? The EPF is a government-backed retirement savings scheme in which both employees and employers contribute a portion of the employee’s salary to build a retirement corpus. 2. What is an inoperative EPF account ? An EPF account becomes inoperative when no contributions are made for three consecutive years after the member retires or turns 55. 3. What is EPFO’s new auto-settlement initiative ? EPFO has approved automatic settlement of inoperative accounts with balances of ₹1,000 or less by transferring the amount directly to the member’s Aadhaar-linked bank account. 4. Why do many EPF accounts become inactive ? Accounts may become inactive due to job changes, retirement without claim submission, lack of updated KYC details, or unawareness among workers. 5. Will auto-settlement be extended to larger balances ? If the pilot project is successful, EPFO may expand the auto-settlement mechanism to cover accounts with balances above ₹1,000 in future phases. |

Our support team will be happy to assist you!

Contact Us

Contact Us  New Batch : 9555124124/ 7428085757

New Batch : 9555124124/ 7428085757  Tech Support : 9555124124/ 7428085757

Tech Support : 9555124124/ 7428085757