- UPSC Exam

- State PCS

- One Day Exam

- Current Affairs

- PT Quiz

- Downlaods

- About Coaching

- Blog

- Videos

|

Syllabus: Prelims GS Paper I : Current events of national and international importance. Mains GS Paper III : Indian Economy and issues relating to planning, mobilization of resources, growth, development and employment. |

Context

The RBI, in its Financial Stability Report, stated that bank NPAs could rise to their highest levels and expressed concerns for future impacts.

Background

The Reserve Bank of India in its Financial Stability Report said over-leveraged non-financial sector, geopolitical tensions and economic losses due to the COVID-19 pandemic are major downside risks to global economic prospects. COVID-19 is expected to create Rs 4-6.2 lakh crore fresh gross NPAs.

Key Findings

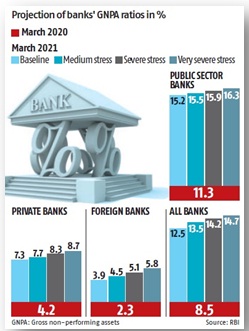

Under the baseline scenario, RBI estimates that the gross non-performing assets (GNPA) of banks- including public, private, and foreign banks in India- may increase from 8.5 percent in March 2020 to 12.5 percent by March 2021.

Further, it expects public sector banks’ GNPA ratio to rise to 15.2 percent by March 2021 from 11.3 percent as of March 2020. Private and foreign banks’ GNPAs are expected to increase from 4.2 per cent and 2.3 per cent to 7.3 per cent and 3.9 per cent, respectively, over the same period.

The overall capital adequacy of banks is also projected to drop from 14.6 percent in March 2020 to 13.3 percent by March 2021, with the core CET-1 (common equity Tier-1) falling to 10.7 percent by March next year from 11.7 percent in 2020. As per regulatory norms, banks are expected to maintain a minimum capital buffer of 9 percent at all times.

Credit Concentration Risk

The study finds that if the largest group-level borrower fails to repay loans, the banking system would face a 6 percent loss of capital, and see bad loans rise from 8.6 percent to 11.9 percent.

If the top two largest group borrowers fail to repay, Indian banks may face 10.9 percent erosion in their capital buffers, and see bad loans jump to 14.7 percent.

If the three largest borrowers fail to repay, the impact would be far larger. Banks may face 15 percent erosion in their capital base, and see bad loans rising to as much as 17 percent.

NBFCs Stress Test

The Report noted that while the bad loan ratio of the Non Banking Finance Company sector declined during successive quarters till December 2019, it surged in March 2020 quarter.

ASEL lll Norms

The Basel Committee on Banking Supervision (BCBS) issued a comprehensive reform package entitled “Basel III: A global regulatory framework for more resilient banks and banking systems” in December 2010 with the objective to improve the banking sector’s ability to absorb shocks arising from financial and economic stress, whatever the source, thus reducing the risk of spillover from the financial sector to the real economy. Under Basel III, a bank's tier 1 and tier 2 assets must be at least 10.5% of its risk-weighted assets.

|

Capital Conservation Buffer: It is the mandatory capital that financial institutions are required to hold above minimum regulatory requirement. As per CCB, Banks will be required to hold a buffer of 2.5% Risk Weighted Assets (RWAs) in the form of Common Equity, over and above Capital Adequacy Ratio of 9%. Types of Bank Capital: Tier 1 capital: It is the bank's core capital and includes disclosed reserves that appears on the bank's financial statements and equity capital. This money is the funds a bank uses to function on a regular basis and forms the basis of a financial institution's strength. Tier 2 capital: It is a bank's supplementary capital. Undisclosed reserves, subordinated term debts, hybrid financial products, and other items make up these funds. Tier 3 capital: It primarily includes NPAs and subordinated loans. |

The declining share of market funding for NBFCs is a concern as it has the potential to accentuate liquidity risk for NBFCs as well as for the financial system

Smaller and mid-sized NBFCs have been shunned by both banks and markets, accentuating the liquidity tensions faced by NBFCs. It observed that in the aftermath of the IL&FS crisis, NBFCs have been facing differentiation in market access and financial conditions, with only the higher rated entities able to raise funds.

RBI, in its stress test for NBFCs found that under the baseline scenario, 11.2 percent of NBFCs would be below minimum regulatory capital requirement of 15 percent.

NBFCs’ total capital adequacy may decline from 19.4 percent to 16.4 percent, and 14 percent of them would be below the minimum regulatory capital requirement.

Moratorium Impact

In March 2020, the Reserve Bank of India had announced a moratorium on the repayment of all term loans for both businesses and households, to ease their burden during the period of the lockdown. Initially allowed for a period of three months, it was subsequently extended till the end of August 2020.

Data from the RBI’s latest financial stability report shows that at the end of April around half of the customers of scheduled commercial banks, accounting for half of the outstanding bank loans, opted to avail of the relief measures extended, underlining the precariousness of their financial position. Public sector banks shouldered a disproportionate burden of the moratorium with roughly two-thirds of borrowers availing of the facility, as opposed to less than half in the case of private banks.

It believes that the impact of moratorium on private NBFCs and Housing Finance Companies can be substantial, with the proportion of assets under moratorium for NBFCs averaging between 39-65 percent as on March 31, based on underlying assets.

Way Forward

The pandemic hit India in a period of growth moderation. The ensuing disruptions in demand conditions and supply chains have been aggravated by global spillovers. However the signs of a gradual recovery from the nationwide lockdown are becoming visible by current data.

Once we enter the post-pandemic phase, the focus would be on calibrated unwinding of regulatory and other dispensations. Financial intermediaries will have to undertake reappraisal of their business models. Asset markets have to adapt to a new normal in a non-disruptive manner.

Also the Banks must proactively augment their capital position to improve their resilience, and that remains the top priority.

Connecting the Dots

Question for Prelims

Which of the following statements is/ are correct regarding Capital Conservation Buffer ?

1. It is the minimum capital that Financial Institutions are required to hold.

2. It helps Financial Institutions in the stressed period.

Select the correct answer using the code given below.

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Question for Mains

How does the nationwide lockdown in the current pandemic posed a serious challenge to the banking sector of the Indian economy ? Suggest necessary measures to make this sector resilient enough.

Our support team will be happy to assist you!

Contact Us

Contact Us  New Batch : 9555124124/ 7428085757

New Batch : 9555124124/ 7428085757  Tech Support : 9555124124/ 7428085757

Tech Support : 9555124124/ 7428085757