- UPSC Exam

- State PCS

- One Day Exam

- Current Affairs

- PT Quiz

- Downlaods

- About Coaching

- Blog

- Videos

|

Syllabus: Prelims GS Paper I : Indian and World Geography-Physical, Social, Economic Geography of India and the World. Mains GS Paper I : Factors responsible for the location of primary, secondary, and tertiary sector industries in various parts of the world (including India). |

Context

The Indian textile sector is under threat due to a less concentrated approach.

Background

The Indian textile industry is now in an era of threats and opportunities. While it enjoys opportunities to gain access to unrestricted markets, it also sees unexpected threats. Since the beginning of 2010, Indian textile industry has been facing one or the other difficulties. Earlier, global economic crisis causing a series of financial difficulties such as closures, less capacity utilizations, layoffs, decline in sales etc. Now, a sharp increase in the textile input prices, and declining exports to US due to competition are putting, the textile industry in a challenging situation. Although, some amount of recovery produced a ray of hope in the minds of textile people.

Indian Textile Industry

The history of textiles in India dates back to nearly 5000 years to the Indus Valley Civilization. The foundations of India’s textile trade with other countries started in the second century BC. India has been trading silk in return of spices.

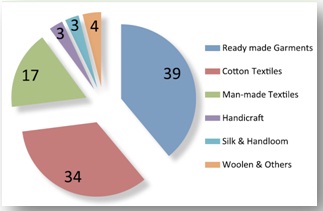

The industry is extremely varied, with hand-spun and hand-woven textiles sectors at one end of the spectrum, while the capital-intensive sophisticated mills sector on the other end. The decentralised power looms/ hosiery and knitting sector forms the largest component in the textiles sector. The close linkage of textiles industry to agriculture (for raw materials such as cotton) and the ancient culture and traditions of the country in terms of textiles makes it unique in comparison to other industries in the country.

India is the world’s second largest producer of textiles and garments and the world’s third largest producer of cotton after China and the USA. The Indian market is also the second largest in terms of consumption of Cotton, after China.

Challenges Faced by the Indian Textile and Apparel Industry

Vision 2025

The domestic textile and apparel industry is projected to grow at a CAGR of 12%, upto 2025, so as to reach a level of US $350 billion. Encouraged by the turnaround in the textile exports, India is expected to grow at a CAGR of 20% for the next 5 years so as to reach a level of US $300 billion.

Government Intervention

Other Initiatives taken by Government of India

Conclusion

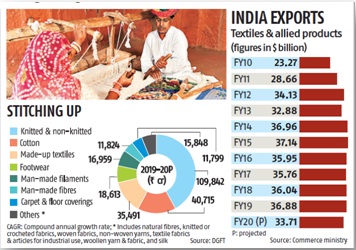

The size of the market in India stood at $162 billion in FY19, including exports worth $37 billion. It has, however, been stagnant since.

According to the Confederation of Indian Textile Industry (CITI), it has the potential to reach $350 billion, including $125 billion in exports by the FY25.

Programs like Skill India and Make-in-India, along with continuous development and growth in the management consulting firms in India for foreign companies, is working in favor of the developments in the Indian textile industry. The access to skilled manpower and a good market for textile products, the industry would become competitive in the global market. With proper market entry strategy for global giants in the market, the future for the Indian textile industry looks promising, buoyed by both strong domestic consumption as well as export demand.

Connecting the Article

Question for Prelims

With reference to the Indian Textile Industry, consider the following statements:

1. India has allowed 100 FDI in textile sector via automatic route.

2. India is a largest exporter of textile and garments.

Which of the statements given above is/ are correct?

(a) 1 only

(b) 2 only

(c) Both 1 and 2

(d) Neither 1 nor 2

Question for Mains

Discuss the Government initiatives to upsurge the Indian textile sector.

Our support team will be happy to assist you!

Contact Us

Contact Us  New Batch : 9555124124/ 7428085757

New Batch : 9555124124/ 7428085757  Tech Support : 9555124124/ 7428085757

Tech Support : 9555124124/ 7428085757